Starting Retirement

You've worked hard to get there. How do you make the most of it?

Our two cents

Our two cents

No matter how far away retirement is, it's important to calculate how much you'll need for a quality life, and immediately start saving to meet that goal.

Reaching retirement is exciting and rewarding. But it can also be a bit scary as you go from earning income to living on your savings.

It takes thought and to make sure you have the money you need to maintain the standard of living you want. The goal is to balance your income and spending while managing your investments wisely so you can enjoy all the good years ahead.

Follow this checklist to make the most of your retirement savings.

Create a regular income stream.

Start by drawing income from sources other than your portfolio. These can include Social Security, pensions, annuities, income property, or part-time work. But, these sources may not cover all your expenses. That's where you tap into your portfolio.

Think of it as writing your own retirement paycheck. As a guideline, consider drawing funds in this order:

- Draw from bonds maturing in the next 12 months, dividends, and interest.

- Take required minimum IRA distributions if you're 73 or older.

- Rebalance your portfolio yearly and sell overweighted assets in your taxable brokerage accounts.

- Sell from your tax-advantaged accounts—first traditional IRAs, then Roth IRAs.

Stay flexible with a laddered approach to bond investing.

To generate income at regular intervals, you can create a bond ladder of high-quality bonds with maturities of 1 year to 5–10 years.

Laddering means buying bonds or notes that mature on different dates. It has two important goals:

- Minimize risk—By staggering maturity dates you avoid getting locked into a single rate. You're protected if rates drop, but you can still capitalize on the opportunity if rates go up. And diversifying your holdings protects you from overall credit risk because you're not lending all of your money to one issuer.

- Manage cash flow—A ladder enables you to manage cash flow for your particular needs. For instance, since many bonds pay interest twice a year, you can structure a monthly income based on coupon payments from laddered bonds by picking bonds with different maturity dates.

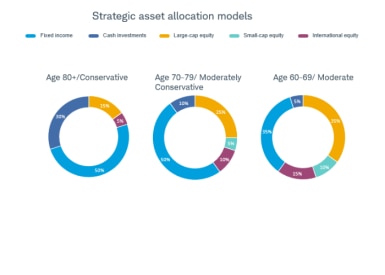

Rebalance your portfolio annually, and review your asset allocation plan.

Rebalancing your portfolio to control risk and stay on track with your goals is important at any age. In retirement, rebalancing can include shifting to a more conservative investing approach.

For instance, early in retirement when you may have higher expenses, you may be willing to take on increased risk in exchange for the potential for more growth. As the years go on, you can adjust your asset allocation to reflect your shorter time horizon.

Source: Schwab Center for Financial Research.

Generate additional cash by selling overweighted asset classes.

You can take care of some of your cash flow needs at the same time you rebalance your portfolio each year. As you reallocate your assets, take out the cash you need. For example, say your target allocation is 60 percent stocks and 40 percent bonds—but your portfolio has drifted to 65 percent stocks and 35 percent bonds. You could cash out what you need from the stock portion and then reallocate what's left over to bonds until you're back on target.

Pay attention to required minimum distributions (RMD).

RMD is the minimum amount that you must withdraw each year. By federal law, traditional, SEP, SIMPLE and Rollover IRA account holders and participants in some qualified retirement plans must begin taking distributions no later than April 1 in the year following the year in which they turn age 73 (70 if you turned 70½ before Jan. 1, 2020). Roth IRAs are not subject to RMD. All shortfalls from the RMD are subject to a 50 percent penalty tax.

While you're required to take your RMD annually, distributions can be aggregated and taken from either one or multiple accounts depending on the type of accounts you own. There are several considerations in calculating your RMD. Talk to your tax advisor or go to IRS.gov.

Periodically review your health and life insurance coverage.

For your own peace of mind, make sure that the health insurance you have is adequate for your needs—and that you're getting the best coverage for your money. Especially when it comes to prescription drug coverage under Medicare, it's smart to review alternate plans during open enrollment periods.

Then there's the question of long-term care insurance (LTC). According to the U.S. Department of Health and Human Services, at least 70 percent of people over age 65 will require some type of long-term care services at some point in their lives. LTC insurance can be expensive. Premiums for LTC vary widely, depending on where the insurance is purchased, the age and health of the buyers, inflation options, and the specific type of insurance purchased. It may not be right for you, but it doesn't hurt to get the facts. Whether you have LTC insurance or not make sure you have a long term plan.

Finally, revisit your life insurance needs. If you no longer have dependents relying on your income or future liabilities or expenses that need to be covered, the money you're putting into life insurance may be better used in another way.

Make sure your estate plan and beneficiary designations are up to date.

If you don't have an estate plan in place, create one now. It will give you peace of mind and may help keep harmony in your family.

If you do have a plan in place, you may want to review it to make sure it's up to date and accessible. Here are some practical considerations:

- Verify that your powers of attorney, will or trust documents are current, especially if there have been any changes in family circumstance such as marriage, divorce or the birth of a grandchild.

- Update named beneficiaries on all retirement accounts, insurance policies, and annuities. (You don't want assets inadvertently going to an ex-spouse.) It's also a good idea to name secondary beneficiaries.

- Make sure a trusted and competent family member or friend knows where important documents and records are kept and has access to them.

Keep learning

Keep learning

Continue to make the most of your retirement years with good retirement account and insurance choices.

Fixed income investments are subject to various risks including changes in interest rates, credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications and other factors.

Investing involves risk, including loss of principal.

Diversification, asset allocation, automatic investing, and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets.